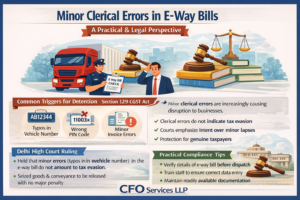

Minor Clerical Errors in E-Way Bills – A Practical & Legal Perspective

1. Executive Summary

Under the GST framework, the movement of goods is closely monitored through e-way bills and supporting documents. Section 129 of the CGST Act empowers tax authorities to detain or seize goods and vehicles where transportation is found to be in contravention of the law.

In recent years, however, a troubling pattern has emerged. Vehicles are increasingly being detained for minor clerical or typographical errors in e-way bills, even where:

- The e-way bill was validly generated,

- The tax invoice and goods details were correct, and

- There was no revenue loss or intention to evade tax.

Such detentions disrupt supply chains, block working capital, and expose businesses to unnecessary litigation.

This newsletter aims to provide clarity by covering:

- The legal framework governing detention under Section 129,

- The distinction between serious non-compliance and harmless procedural lapses,

- Recent judicial trends offering protection to genuine taxpayers, and

- Practical steps businesses can take to minimise risk

2. Statutory Framework – Section 129 of the CGST Act

Section 129 provides that where goods are transported in contravention of the provisions of the GST law, the proper officer may detain or seize:

- The goods, and

- The conveyance carrying such goods,

until payment of applicable tax and penalty or furnishing of security.

For movement of goods exceeding ₹50,000 in value, the law requires the following documents:

- A valid tax invoice or delivery challan,

- A properly generated e-way bill under Rule 138,

- Relevant transport documents such as LR or GR.

If the owner does not come forward for release, the law permits levy of penalty up to 200% of the tax payable (or prescribed amounts for exempt goods).

Core expectation of the law:

The e-way bill should correctly and truthfully reflect the underlying transaction.

3. Procedural vs Substantive Errors—Ground-Level Reality

- Common Triggers for Detention

In practice, enforcement actions under Section 129 are often initiated on grounds such as:

- Incorrect or incomplete particulars in the e-way bill (PIN code, vehicle number, etc.),

- Alleged mismatch between invoice and e-way bill details,

- Allegation that no valid e-way bill existed at the time of interception.

What is increasingly concerning is that vehicles are sometimes detained solely for minor clerical or typographical errors, even when:

- The e-way bill was generated before movement,

- Invoice value, GSTIN, and description of goods matched perfectly,

- All prescribed documents were physically or electronically available.

This approach has created uncertainty and anxiety for businesses and transporters, who are left vulnerable to operational disruptions despite bona fide compliance.

4. Judicial Trends and Protective Jurisprudence

During 2024–25, judicial thinking has shown a clear and consistent shift towards protecting genuine taxpayers from excessive enforcement action where lapses are purely technical.

Courts have repeatedly emphasized that Section 129 is meant to curb tax evasion—not to penalize human error. The presence (or absence) of intent to evade tax (mens rea) has emerged as the decisive factor.

– Protection in Cases of Bona Fide Errors

Judicial pronouncements have broadly settled the following principles:

- Clerical Errors in E-Way Bills

Minor clerical mistakes—such as an incorrect or partially incorrect vehicle number—do not justify detention or penalty where the goods, invoice, and transaction details otherwise match and there is no indication of tax evasion. - Typographical Error in Document or Invoice Number

Where the only discrepancy is a one-digit mismatch in the invoice or document number mentioned in the e-way bill, such an error has been treated as a technical lapse insufficient to trigger penal proceedings under Section 129. - Wrong PIN Code

An incorrect PIN code, by itself, has been recognised as a clerical error when all other details (consignor, consignee, GSTIN, goods) are accurate and the transaction is genuine. - Incorrect Dispatch Location

Errors relating to dispatch location or place of dispatch, arising from data entry mistakes and not affecting tax liability, have been held inadequate to sustain seizure or penalty. - E-Way Bill Generated Before Interception

Where the e-way bill was generated prior to interception, courts have consistently held that penal action cannot be sustained, as timely generation reflects bona fide conduct and negates any presumption of tax evasion.

Underlying message:

Mechanical enforcement without examining intent, revenue impact, and transaction genuineness is legally unsustainable.

– Regulatory Guidance – CBIC Circular (2018)

Reinforcing this approach, the CBIC issued Circular No. 64/38/2018, clarifying that Section 129 proceedings should not be initiated in cases involving:

- Minor spelling mistakes where GSTIN is correct,

- PIN code errors where locality is identifiable and e-way bill validity is unaffected,

- Minor address discrepancies,

- Small mistakes in invoice or document numbers.

In such cases, the law contemplates a nominal penalty under Section 125 (generally ₹500 or ₹1,000), rather than detention and seizure under Section 129.

5. Practical Compliance & Risk Mitigation

From both a compliance and litigation standpoint, disciplined processes are essential.

- Before Dispatch

- Generate the e-way bill well before commencement of movement.

- Ensure complete consistency across:

- Tax invoice,

- E-way bill details (GSTIN, name, address, PIN),

- Transport documents (LR/GR).

- If any error is detected before movement, cancel and regenerate the e-way bill within the permitted 24-hour window under Rule 138(9).

- During Interception

If a vehicle is intercepted:

- Produce all documents immediately invoice, e-way bill, packing list.

- Highlight the time of e-way bill generation, especially where it predates interception.

- Demonstrate transaction genuineness through delivery challans, payment records, or internal transfer documentation.

- Documentation Discipline

- Implement internal verification checklists.

- Train transporters on timely updating of vehicle details.

- Maintain audit trails evidencing bona fide dispatch and compliance workflows.

6. Conclusion & Recommendations

The evolving judicial and regulatory landscape clearly signals a pro-business and pragmatic interpretation of Section 129. Procedural lapses, in the absence of tax evasion intent or revenue loss, should not attract severe penal consequences.

Key takeaways for businesses:

- Treat disputes arising from clerical errors as legal risk events requiring immediate documentation and written explanation.

- Strengthen SOPs to ensure accuracy and timely correction of e-way bills.

- Assertively rely on judicial trends and CBIC clarifications to safeguard interests where detention is triggered by trivial mistakes.

In essence:

GST enforcement is moving towards fairness and proportionality. Businesses that maintain documentary integrity and respond decisively can effectively protect themselves from unjust detention and penalties.

If you are facing detention of goods or vehicles under Section 129 of the CGST Act, professional GST advisory support can help you navigate the release procedure and penalties.